Simply closer

to financial markets

25th MathFinance Conference

Thu. 18th & Fri. 19th September 2025

About the Conference

MathFinance will bring together the quantitative finance community at its 25th anniversary conference.

This is a unique opportunity to bridge the gap between investment banking and academic research in mathematical finance.

The 25th MathFinance Conference will take place at Reichenstein Castle near Frankfurt in a special atmosphere.

Not to mention the fantastic dinner with a view to the Rhine River on Thursday evening.

Finally, the MathFinance conference is all about cutting-edge research and brand-new practical applications.

What to expect?

During the 25th MathFinance Conference we will explore the themes of derivatives pricing and risk management, crypto exotics markets, machine learning, smart Greeks, climate finance, and much more.

A symposium on Energy Derivatives is organized by Karel in’t Hout,

To conclude, we are proud to announce that this year we will be welcoming the world’s leading experts in quantitative finance.

Conference Venue

Burg Reichenstein

Burgweg 24

55413 Trechtingshausen

T: +49 (0) 6721 6117

E: info@burg-reichenstein.com

W: www.burg-reichenstein.com

Burg Reichenstein is owned and run by the Puricelli family and their descendants, who will host us within its ancient walls.

An outdoor bowling alley can be used after dinner in the castle garden.

How to reach the 25th MathFinance Conference

From Frankfurt Main Station (Hbf) by train:

=> https://int.bahn.de/en

From the Frankfurt-Airport to Trechtingshausen:

Agenda

Day 1

Thursday, 18th September 2025

(Coffee break from 10:00)

10:30 Registration & Opening Remarks day 1: Uwe Wystup, MathFinance

10:50 Morning Session – Chair: Karel In’t Hout

Mini-Symposium on Energy Options

11:00 A Local Volatility Model for Commodity Forwards: Nils Detering, Heinrich Heine University Düsseldorf

11:30: Numerical Valuation of European Options under Two-Asset Infinite Activity Exponential Lévy Models: Massimiliano Moda, University of Antwerp

12:00 Numerical Methods for Solving PIDEs Arising in Swing Option Pricing under a Two-Factor Mean-Reverting Model with Jumps: Mustapha Regragui, University of Ghent

12:30 Power and Emissions Trading: Erik Vynckier

13:00 Photo Session & Lunch Break

Afternoon Session – Chair: Jörg Behrens

14:00 Champion vs. Challenger – How to Deconstruct an AI Challenger Model to Validate Traditional Credit Scoring? Andree Heseler, mex consulting

14:30 Arbitrage-Free Encoder-Decoder Term Structure Models: Rolf Poulsen, University of Copenhagen

15:00 Blockchain in Securities Settlement: A German Perspective on the Status Quo: Benjamin Schaub, Plutoneo

15:30 Coffee Break

16:00 TBA: TBA, Deloitte

16:30 Re-evaluating Short- and Long-Term Trend Factors in CTA Replication: A Bayesian Graphical Approach: Eric Benhamou, AI for Alpha

17:00 OTC Derivatives Trades Visualized: Wojciech Mucha & Toru Tokoyoda, Enterprai

17:30 Solved After 2000 Years of Struggle: Just Intonation: Hans-Peter Deutsch, Musical Tonality

18:00 Ending Remarks day 1: Uwe Wystup, MathFinance

19:00 Reception and Conference Dinner

All times in Central European Summer Time

Day 2

Friday, 19th September 2025

08:30 Registration

Morning Session – Chair: Martin Simon

09:00 Conformal Statistics-Informed Neural Emulators in Financial Risk Applications: Martin Simon, Frankfurt University of Applied Sciences & MathFinance

09:30 Affine Modelling in Term Structure Markets with Stochastic Discontinuities: Thorsten Schmidt, University of Freiburg & MathFinance

10:00 The Schrodinger Problem for the Local Volatility in Production: Adil Reghai, Abu Dhabi Investment Authority (online)

10:30 Architectures for Regulated DLT Markets: A Deep Dive into Smart Contracts and Delivery vs. Payment: Bert Staufenbiel & Tim Meirer, KfW Frankfurt

11:00 Coffee Break

11:30 Hybrid Computing: Bernd Ulmann, anabrid GmbH

12:00 Market Data Meets Cloud Computing: Streamlining Complex Financial Calculations: Mauricio González and William Bierds, bccg

12:30 Structured OTC FX – Evolution of Platforms from Single-Dealer to Multi-Dealer: Milind Kulkarni & Nitish Bandle, FinIQ

13:00 Lunch Break

Afternoon Session – Chair: Uwe Wystup

14:15 On the Pricing of Double Barrier Options under Stochastic Volatility Models: Probabilistic Approach: Yerkin Kitapbayev, Khalifa University, UAE

14:45 Path-dependent PDEs for Rough Volatility: Jack Jacquier, Imperial College London

15:15 Analysis of volatility strangles via Normalizing Volatility Transforms: Parviz Rakhmonov & Nathan Pariser, Marex Solutions London

15:45 Coffee Break

16:15 Optimal exit from Uniswap v3 and best expected return for a liquidity provider: Emmanuel Gobet, Sorbonne Université, Paris

16:45 Uninformative Portfolio Choice: Model-Free Asset Allocation: Jan Vecer, Charles University Prague

17:15 Some Financial Applications of the Functional Itô Calculus: Bruno Dupire, Bloomberg

17:45 Closing Remarks: Uwe Wystup, MathFinance

All times in Central European Summer Time

MathFinance will make video and audio recordings during the event. By registering, the participant expressly agrees that MathFinance may make and publish recordings of his or her person.

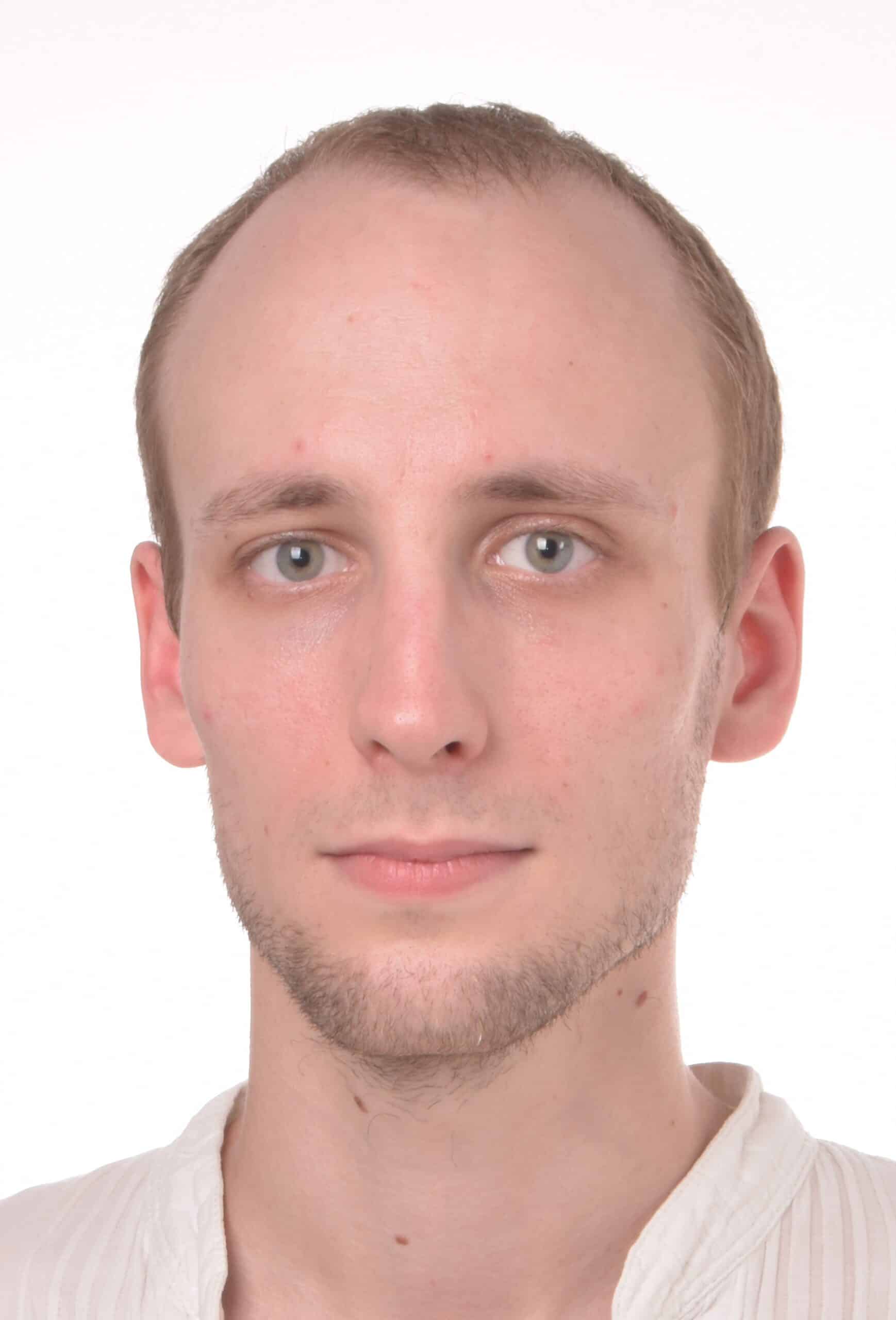

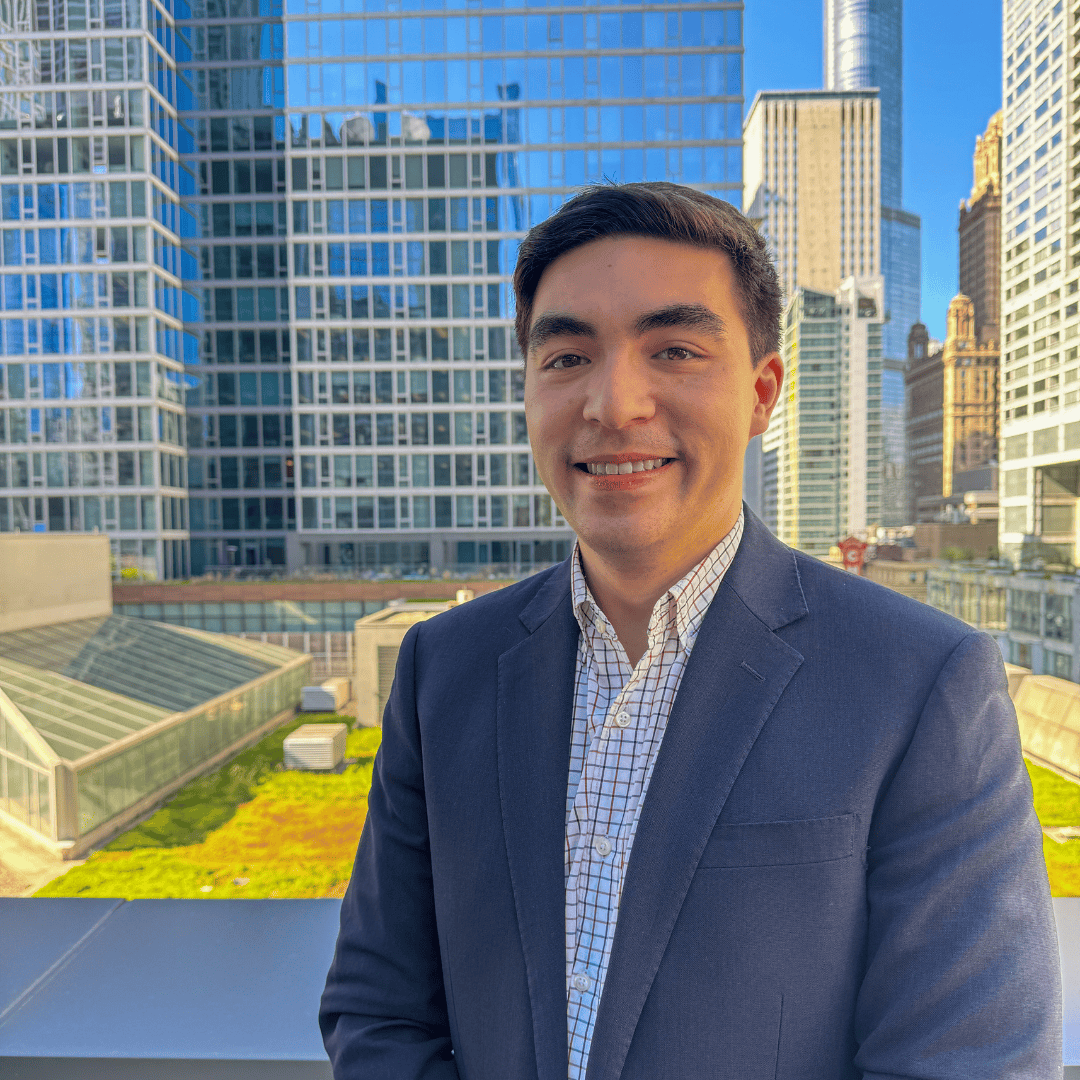

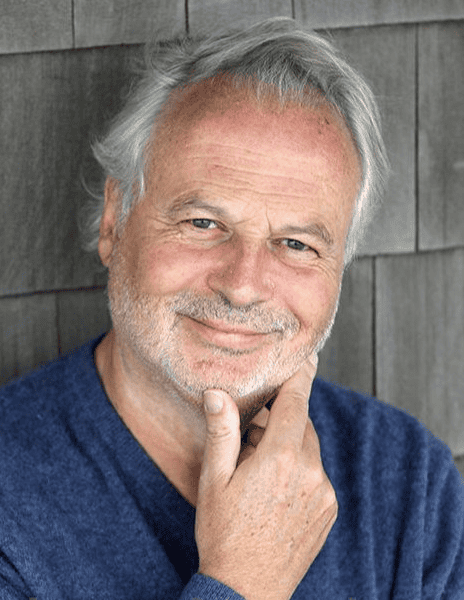

Conference Speakers

Confirmed speakers and panelists. Click on the images below to explore abstracts and biographies.

Minisymposium on Energy Options

Standard-Price-Ticket

including conference dinner, without hotel room

Burg Reichenstein

Burgweg 24

55413 Trechtingshausen

T: +49 (0) 6721 6117

E: info@burg-reichenstein.com

W: www.burg-reichenstein.com

Land & Golfhotel Stromberg

Am Buchenring 6

55442 Stromberg/Bingen

T: +49 (0) 6724/600-0

E: info@golfhotel-stromberg.de

W: www.golfhotel-stromberg.de

For participants who are staying at the Land & Golfhotel Stromberg: We offer you a free shuttle service to Burg Reichenstein.

Burg Reichenstein

Shuttle-Service

We offer you a free Shuttle-Service from Stromberg Hotel to the burg Reichenstein.

Any questions concerning your accommodation or your ticket?

Please do not hesitate to contact us at:

conference@mathfinance.com

The standard ticket price includes a conference dinner in the castle.

(without accommodation)

Conference Tickets

Date

18. & 19. September 2025

Time

10:00 -18:00 CET

early bird

Until June 30th

1.250,00 €

Standard ticket

Includes conference dinner

(without hotel room)

1.345,00 €

Academic rate

475,00 €

Groups

2.500,00 €

Groups

3.750,00 €

Specials

Sponsor … only upon request

Invited guest … only upon request

Online tickets … only upon request

Student rate … only upon request

For requests please send

an E-Mail to

Sponsors

We are proudly supported by:

Affiliate Partners

Media Partners

Photo Gallery 2025

MathFinance Conference – Symposium Team with participants

MathFinance Conference: Uwe Wystup & Bruno Dupire

MathFinance Conference: Uwe Wystup and a group of students

MathFinance Conference – networking

MathFinance Conference – Emmanuel Gobet

MathFinance Conference – William Bierds & Rittik Wystup

MathFinance Conference – Benjamin Schaub

MathFinance Conference – Jack Jacquier

MathFinance Conference: Karl Hofmann

MathFinance Conference: Jörg Behrens

MathFinance Conference: Rolf Poulsen

MathFinance Conference_Deryan Ulevinov

MathFinance Conference_Eric Benhamou

MathFinance Conference_Erik Vynckier

MathFinance Conference_Hans-Peter Deutsch

MathFinance Conference_Uwe Wystup and Stuart Deel-Smith

MathFinance Conference_Jan Vecer

MathFinance Conference_Bernd Ulmann

MathFinance Conference_Bert Staufenbiel_und_Tim_Meirer

MathFinance Conference_Karel in’t Hout

MathFinance Conference_Martin Simon

MathFinance Conference_Andree Heseler

MathFinance Conference_Parviz Rakhmonov

MathFinance Conference_Thorsten Schmidt

All photographs by Bettina Roth