Editorial

XOF

XOF is not the exit for Offenbach, nor an old-fashioned precious metal, but the currency code for the CFA Franc. The West African CFA franc is the currency of eight independent states in West Africa: Benin, Burkina Faso, Guinea-Bissau, Ivory Coast, Mali, Niger, Senegal and Togo. The acronym CFA stands for Communauté Financière d’Afrique (“Financial Community of Africa”) or Communauté Financière Africaine (“African Financial Community”). The currency is issued by the BCEAO (Banque Centrale des États de l’Afrique de l’Ouest, “Central Bank of the West African States”), located in Dakar, Senegal.

Interestingly, it was practically pegged to the EUR until summer 2017, as it was formerly pegged to the French Franc, see Figure 1. After this there have been some jumps when the peg has been moved.

Figure 1: EUR/XOF historic rates over the last two years; sourced from Eikon

A peg should imply that the XOF interest rate must match the EUR interest rate, as otherwise there could be an arbitrage opportunity: buy XOF for your EUR, deposit them with the BCEAO, then change back to EUR after a month at presumingly the same spot reference and finally get the interest rate on the EUR that you think you deserve.

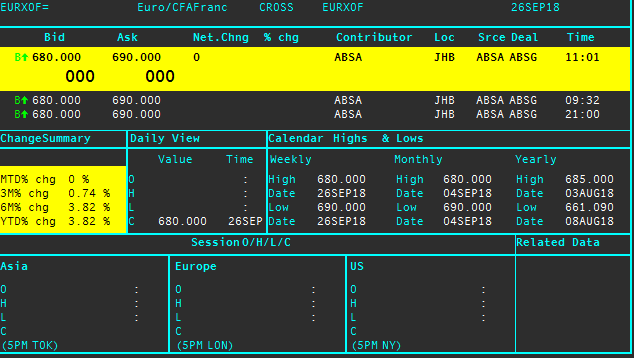

Figure 2: EUR/XOF spot quotation seen in Reuters Eikon

How about market data: I see a spot of 680 – 690 bid – offer by ABSA bank in Johannesburg in Eikon (Figure 3), but also a spot of 648.90 – 657.22 on Eikon’s Euro/CFA France page EURXOF (Figure 2), XE.com shows a 10-year low of 655.88259, a 10-year high at 656.01663, and a closing spot of 655.957. SuperDerivatives’ FX Option pricer shows a spot reference of 652.47 CFA Franc per EUR on 28 September 2018, so it may not have updated the spot since summer 2017. While XOF seems pegged to the EUR, there is a lively forward market with quotes as shown in Figure 2.

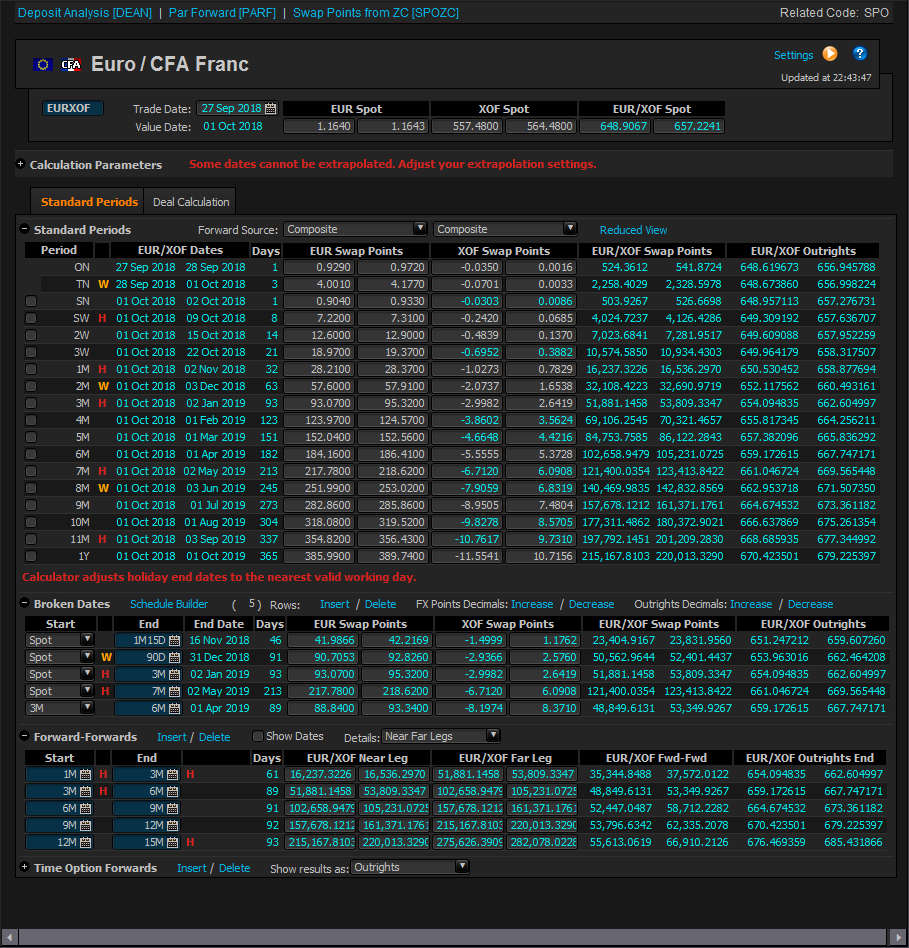

Figure 3: EUR/XOF forward rates sourced from Eikon

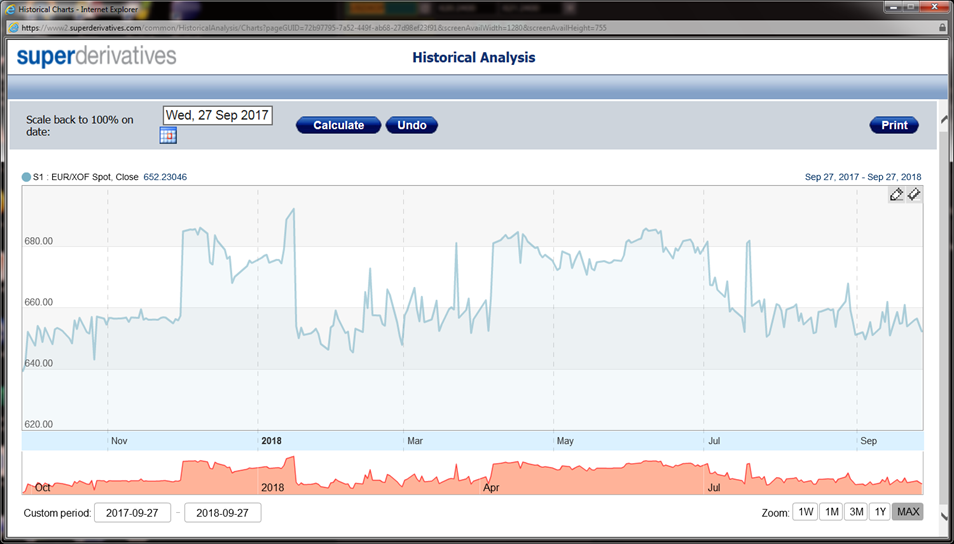

The historic spot as indicated by SuperDerivatives is shown in Figure 4. Notably it appears different from the spot recorded by Reuters in Figure 1.

Figure 4: EUR/XOF historic spot sourced from SuperDerivatives

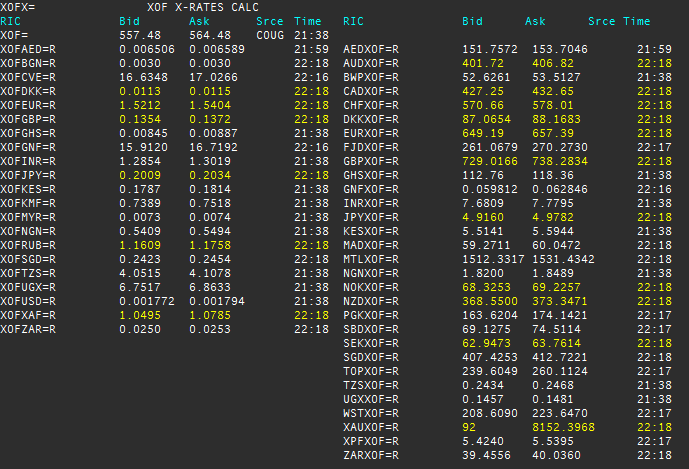

It remains opaque to me where the spot is and also how the historic spot is recorded as there are obvious differences in XE, Reuters and SuperDerivatives. However, the spot rate appears to be pegged with a bid-offer of 8 XOF per EUR as per observed quote in Eikon, higher fluctuations in SuperDerivatives probably due to illiquid and scattered transactions. Calculated cross rates are exhibited in Figure 5. Notably, even if the CFA Franc is expected to be closer to the Euro, the EUR/XOF exchange rate is calculated as a cross rate between EUR/USD and USD/XOF.

Figure 5: XOF calculated cross rates in Eikon

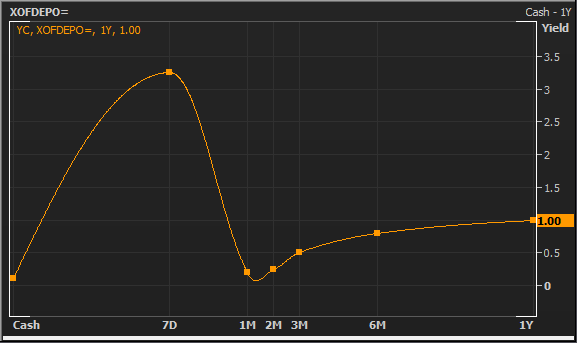

Turning to the interest rates, we see a one-year deposit rate of -0.475% in EUR in SuperDerivatives, keeping in mind that deposit rates in the FX option pricer are pre-calculated to match the FX forward. The XOF interest rate shown in SuperDerivatives is +2.781%. Reuters calculates a rate curve in Figure 6.

Figure 6: XOF yield curve of 27 Sept 2018, calculated in Eikon

The Central African Central Bank shows a rate of +2.95% on their web page https://www.beac.int/ . While the forward rates in Figure 2 seem to reflect the difference of interest rate in principle, the pegged spot would actually call for an arbitrage opportunity, especially for a 1-week deposit when we consider the yield curve.

The CFA France is a very interesting example of distortions in the market. The credit fan club will now probably start calculating the probability of the BCEAO defaulting. The difference of rates is a strong indication that the peg will have to break over and over again.

I didn’t find any volatility data; currently in Africa we see only volatilities for ZAR (South African Rand) and KES (Kenyan Shilling). XOF may not need any FX options, as one can trade options on EUR instead. Otherwise, the relevance of the West African economy would actually call for options, too. Let’s see.

Good luck with your interest rate arbitrage!

Uwe Wystup

Managing Director of MathFinance

Upcoming Events

FX EXOTIC OPTIONS IN FRANKFURT 2018

December 10 – 12, 2018

Lecturer: Prof. Dr. Uwe Wystup

This advanced practical three-day course covers the pricing, hedging and application of FX exotics for use in trading, risk management, financial engineering and structured products.

FX exotics are becoming increasingly commonplace in today’s capital markets. The objective of this workshop is to develop a solid understanding of the current exotic currency derivatives used in international treasury management. This will give participants the mathematical and practical background necessary to deal with all the products on the market.

Learn more about the training or register directly.

MATHFINANCE CONFERENCE 2019

Save the date for the next Conference on April 08 & 09, 2019 in Frankfurt

With a blend of world renowned speakers from academia and industry providing cutting-edge research and brand new practical applications this event is a must for everyone in the quantitative financial industry. We expect around 100 delegates ensuring a unique networking opportunity which should not be missed.

More information on the conference and registration to soon follow.

Careers

MathFinance Openings

Senior Quant/ Consultant

We are looking for senior quant / consultant in the areas of

Insurance

- Actuary with 5 to 7 years of experience in insurance or re-insurance

- Experience in quantitative Risk Management in relation to regulatory issues (Solvency II)

- Experience in Capital Management

Banking

- Quant with 5 to 7 years of experience in Banking, ideally in Trading

- Experience in quantitative Risk Management in relation to regulatory issues (Basel III)

- Experience in Capital Management

Investment

- Quant with 5 to 7 years of experience in Asset Management (Funds, Insurance and Family Offices), ideally with emphasis on Risk Management

- Experience in quantitative Risk Management in relation to regulatory issues (German KAGB and KARBV)

Please send us your CV to recruitments@mathfinance.com

Junior Quant

Do the following apply to you?

- Master degree or diploma in (business) mathematics or physics

- PhD or CFA is a bonus

- First experiences in mathematical finance is desirable

- Very good programming skills, e.g. C++, Python or Matlab

- Good language skills in German and English

- Outstanding analytical skills and a problem-solving attitude

- High motivation to develop your knowledge and skills

- Good communication skills and team spirit

Then we would like to hear from you. Please send us your CV to recruitments@mathfinance.com