Editorial

FX Volatility Market Data: How Independent are 10-Delta Quotes for Risk Reversals and Butterflies?

The information of the FX volatility surface is contained in a small set of market quotes as you would find them at brokers: ATM volatility, 25-Delta Risk Reversals (RR25), 10-Delta Risk Reversals (RR10), 25-Delta Butterflies (BF25) and 10-Delta Butterflies (BF10). At least, this is what some people say or write – including myself. In some exceptional cases, we will also have information of the 5-Delta levels.

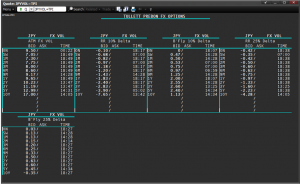

For example Tullett Prebon provides a set of such quotes for USD/JPY volatilities for tenors up to 10 years:

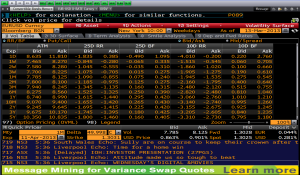

Bloomberg provides similar information on its OVDV pages, for example EUR/USD below.

SuperDerivatives, interestingly, does not view 10-delta quotes as valid input for their volatility smile.

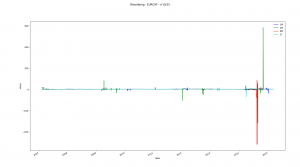

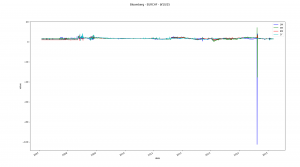

A question one might ask is how independent the 10-delta quotes actually are. For this we have analyzed historic time series of risk reversals and butterflies in EUR/CHF for the period 2007 to 2016. As a result we plot the ratios of BF25/BF10 and RR25/RR10 in the following two graphs.

My interpretation for both risk reversals and butterflies is that the 10-delta quotes appear to be a constant multiple of the 25-delta quotes in most cases, even for different maturities. Minor exceptions from this rule are only observable on special market event dates like 15 January 2015, when the Swiss National Bank terminated the 1.2000 protection level in EUR/CHF.

It appears that sometimes there are independent 10-delta quotes, but when there aren’t any such quotes, the data providers or brokers simply calculate the missing quotes using a constant ratio approach. After all, clients tend to complain more if information is missing or outdated, but less if there is an entry in the matrix, which can’t be classified wrong in any obvious way. That way, the SuperDerivatives approach not using 10-delta quotes alltogether and not listing volatility smile quotes for maturities beyond two years probably reflects more of the market reality.

We conclude that 10-delta quotes are overrated. Most of the time they appear to be simply calculated from 25-delta quotes just to fill the table. As a consequence, when we try to fit a parametric smile curve through a set of given points, the weight assigned to the 10-delta quotes can be smaller than the ATM or 25-delta quotes. It is pointless to force precision and hit a 10-delta quote exactly, which is just a number somebody else has calculated.

Homework: find the ratios.

Uwe Wystup, Managing Director of MathFinance

Upcoming Events

MATHFINANCE CONFERENCE 2018

Date: April 16 – 17, 2018

Venue: Frankfurt School of Finance & Management, Adickesallee 32-34, 60322 Frankfurt am Main

MathFinance Conference has been successfully running since 2000 and has become one of the top quant events of the year. The conference is specifically designed for practitioners in the areas of trading, quantitative and derivatives research, risk and asset management, insurance, as well as academics.

As always, we expect around 100 delegates both from the academia and the industry. This ensures a unique networking opportunity which should not be missed. A blend of world renowned speakers ensure that a variety of topics and issues of immediate importance are covered.

Our confirmed speakers for 2018 include:

- Dr. Tomasz Bielecki (Illinois Institute of Technology): tba

- William McGhee (NatWest Markets): Machine Learning in Quantitative Finance

- Jessica James (Commerzbank): A deep dive into the causes of the cross currency basis

- Prof. Rolf Poulsen (University of Copenhagen): How Accurately Did Markets Predict the GBP/USD Exchange Rate Around the Brexit Referendum?

- Adil Reghaï (Natixis): The fair pricing under local stochastic volatility

- Artur Sepp (Julius Bär): Applications of Machine Learning for volatility prediction

- Uwe Wystup (MathFinance): FX Volatility 101 Exam

Besides interesting talks there will be a Mini-Symposium on “Computational Finance” organized by Prof. Karel in’t Hout. More details of the agenda will be published soon.

We will also have a call for a Poster Session soon. An independant jury consisting of Prof. Dr. Natalie Packham, Professor of Mathematics and Statistics, Berlin School of Economics and Law, Dr. Michael Einemann, Risk Methodology Specialst, Deutsche Bank AG and Prof. Dr. Andrija Mihoci, Professor of Statistics and Econometrics, Technical University Cottbus will nominate the best five posters to be presented at the conference. The winner will receive free admittance to the whole conference. Details on our poster session will be published in our November Newsletter.

Please click here for registration (single / group):

Single tickets are priced at our prime price of EUR 735 (+VAT) which ends on January 31, 2018.

Academics pay 525 EUR (+VAT) at all times. We kindly ask for proof of your affiliation.

Group prices (3 or more from the same institution) are at EUR 735 (+VAT) pp.

Discounted price of EUR 840 (+VAT) is valid from February 1 until February 28, 2018.

Regular price from March 1, 2018 is EUR 1.050 (+VAT).

Details of the conference on our website to follow soon.

MATHFINANCE SEMINAR: FX EXOTIC OPTIONS

Date: November 29 – December 01, 2017

Venue: Frankfurt School of Finance & Management, Adickesallee 32-34, 60322 Frankfurt am Main

Lecturer: Prof. Dr. Uwe Wystup

This advanced practical three-day course covers the pricing, hedging and application of FX exotics for use in trading, risk management, financial engineering and structured products.

FX exotics are becoming increasingly commonplace in today’s capital markets. The objective of this workshop is to develop a solid understanding of the current exotic currency derivatives used in international treasury management. This will give participants the mathematical and practical background necessary to deal with all the products on the market.

Learn more about the training or register directly.

WINTER SCHOOL, LUNTEREN, THE NETHERLANDS

The 17th Winter School on Mathematical Finance will take place on January 22-24, 2018 in Congrescentrum De Werelt, Lunteren, The Netherlands.

Special topics are Extreme Risks, and Algorithmic and high-frequency trading. There will be two mini courses of 5 hours each by Emmanuel Gobet (Ecole Polytechnique, Palaiseau) and Sebastian Jaimungal (University of Toronto). Special invited lectures will be given by Beatrice Acciaio (London School of Economics), Giulia Di Nunno (University of Oslo), and Martino Grasselli (Pôle Universitaire Léonard de Vinci, Paris La Defense and University of Padua). Four short lectures complete the program.

Registration and further information on https://staff.fnwi.uva.nl/p.j.c.spreij/winterschool/winterschool.html

Careers

MathFinance Openings

Senior Quant/ Consultant

We are looking for senior quant/ consultant in the areas of

Insurance

- Actuary with 5 to 7 years of experience in insurance or re-insurance

- Experience in quantitative Risk Management in relation to regulatory issues (Solvency II)

- Experience in Capital Management

Banking

- Quant with 5 to 7 years of experience in Banking, ideally in Trading

- Experience in quantitative Risk Management in relation to regulatory issues (Basel III)

- Experience in Capital Management

Investment

- Quant with 5 to 7 years of experience in Asset Management (Funds, Insurance and Family Offices), ideally with emphasis on Risk Management

- Experience in quantitative Risk Management in relation to regulatory issues (German KAGB and KARBV)

Please send us your CV to recruitments@mathfinance.com

Junior Quant

Do the following apply to you?

- Master degree or diploma in (business) mathematics or physics

- PhD or CFA is a bonus

- First experiences in mathematical finance is desirable

- Very good programming skills, e.g. C++, Python or Matlab

- Good language skills in German and English

- Outstanding analytical skills and a problem-solving attitude

- High motivation to develop your knowledge and skills

- Good communication skills and team spirit

Then we would like to hear from you. Please send us your CV to recruitments@mathfinance.com