Editorial

Trade Idea for the Turkish Lira

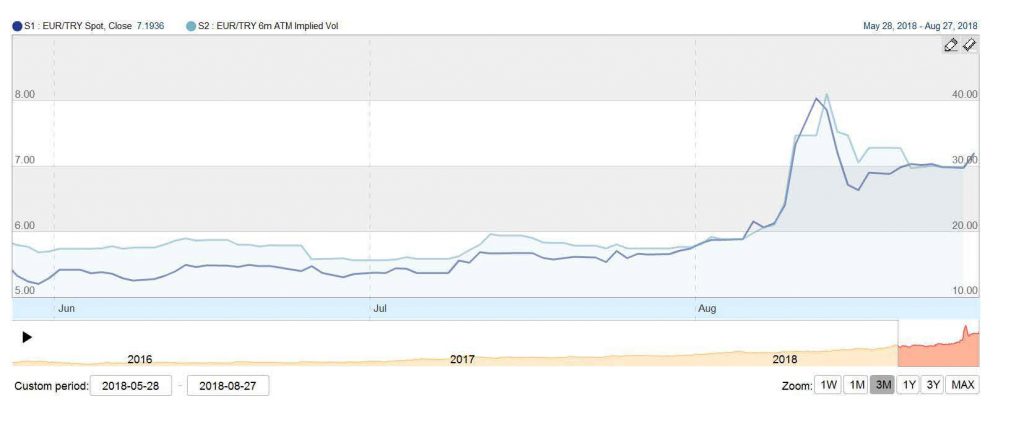

The price of a EUR in Turkish Lira (EUR-TRY) has moved up from 5.00 to above 7.00 in the last 3 months, a rise by more than 40%. For currencies, even for emerging markets’ currencies, this is a dramatic move. Along with the spot rise, implied volatilities for 6-months options have risen from 15% to 30%, see Figure 1. How can a proprietary trader benefit from a view that EUR-TRY will stay above 7.00 in 6 months, but not cross the level of 12.00? We don’t want to spend a lot of money, i.e. we are looking at a zero-cost strategy; and we would like to run our strategy on a margined account.

Figure 1: historic spot and 6M ATM volatility for EUR-TRY in summer 2018; source: SuperDerivatives

An idea that comes to my mind is a ratio call spread: we buy a 6-months EUR call struck at 7.00 for EUR 1 M, and sell a 6-months call struck at 12.00 for EUR 10 M (leverage factor 10, no kidding). On market data of 27 August (spot reference 7.20, ATM volatility 30.40%, 25-delta risk reversal 8.45%, 25-delta butterfly 1.581, EUR money market rate of -0.508%, forward rate 8.30895, implied TRY money market rate 29.549%, long call mid volatility 27.36%, short call mid volatility 41.58%), the mid price would be -4,000 EUR, so could trade a zero-cost for the investor and a sales margin of EUR 4,000 for the bank.

Scenario 1 Lira strengthening: if the Lira becomes stronger, i.e. EUR-TRY drops below 7.00 in 6 months, then both call options are out of the money, so no payoff is generated. For a zero-cost initial premium, this is acceptable. We’ll try again in the next currency crisis.

Scenario 2 Lira weakening further: if the Lira becomes weaker, i.e. EUR-TRY rises to a level of, say 10.00, then the long EUR call pays off 3 M TRY, worth EUR 300,000. The short EUR call is out of the money. Happy days.

Scenario 3 Lira weakens dramatically: if the Lira becomes dramatically weaker, i.e. EUR-TRY crosses the 12.00 level, then also the short EUR call is in the money, and the position can theoretically generate an unlimited loss. However, the point of the strategy is that this scenario is considered highly unlikely. And if it really goes wrong, we simply sue the bank.

Overall, this may appear very attractive to investors with a decent enthusiasm about leverage investing. It works, because the forward is going up, and consequently, the short call is worth a lot and additionally is priced with a high volatility because of a risk reversal of 8.45% in favor of EUR calls.

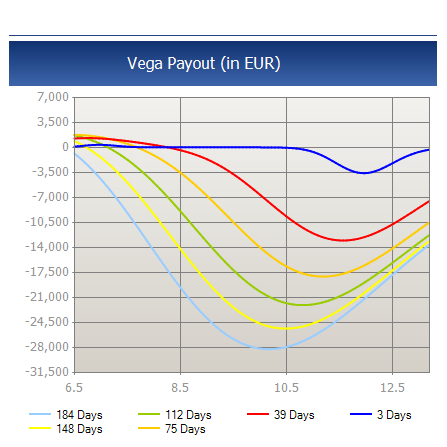

However, the risk of the strategy for the selling bank is very high because of the investor’s high leverage and short option position with unlimited potential losses. Consequently, this would only be traded if the investor maintains a margined account. For example, and for simplicity, if the risk is 5 times the strategy’s vega, then the initial margin would be 5 time EUR 13,800, so EUR 69,000. This would be redeemed in scenario 1, and for scenario 2, the ROI is still in excess of 400% (800% p.a., as a clever sales guy would point out). The problem is that as spot rises, vega increases as can be seen in Figure 2, thus the investor can expect margin calls in a situation that he actually hopes to occur. If he can’t meet the margin calls, his position will likely be force-closed with a loss. How much margin is required on the way can be found out only if we know the method the margin for the structure is calculated. The five-vega rule-of-thumb isn’t actually too bad, but obviously simplified.

Figure 2: vega profile of the ratio 10 call spread in EUR-TRY of the 6 months life time.; source: SuperDerivatives

You won’t believe how many such simplified margin calculators were in place in the last decade. In fact, I remember a Turkish trader who had taken exactly this view and position in the beginning of 2008, when he strongly believed that USD-TRY would rise from 1.20 to 1.60 within 6 months. And since he had so much of fun with his ratio call spreads, he had a whole portfolio of similar trades. The margin had been calculated a linear combination of vega and gamma, so just an inch more complex than my simplified approach.

He could not meet his margin call that had come daily for sizes of USD 500k, so his position was force-closed. He had envisioned a USD 20 M profit, but ended up with a USD 20 M loss. He sued the bank, and ended up in a not very comfortable settlement of his case at the commercial court in London. I just thought I share this example of the past with you, as many investors might consider similar investments at the current market. I am not saying not to do it, but you might want to choose your law firm and experts wisely.

Uwe Wystup

Managing Director of MathFinance

Upcoming Events

FX EXOTIC OPTIONS IN FRANKFURT 2018

December 10 – 12, 2018

Lecturer: Prof. Dr. Uwe Wystup

This advanced practical three-day course covers the pricing, hedging and application of FX exotics for use in trading, risk management, financial engineering and structured products.

FX exotics are becoming increasingly commonplace in today’s capital markets. The objective of this workshop is to develop a solid understanding of the current exotic currency derivatives used in international treasury management. This will give participants the mathematical and practical background necessary to deal with all the products on the market.

Learn more about the training or register directly.

MATHFINANCE CONFERENCE 2019

Save the date for the next Conference on April 08 & 09, 2019 in Frankfurt

With a blend of world renowned speakers from academia and industry providing cutting-edge research and brand new practical applications this event is a must for everyone in the quantitative financial industry. We expect around 100 delegates ensuring a unique networking opportunity which should not be missed.

More information on the conference and registration to soon follow.

D-FINE HACKATHON | 19. – 21. OKTOBER 2018 | DREISCHEIBENHAUS DÜSSELDORF

Du liebst es Daten zu analysieren und daraus innovative Ideen zu entwickeln? Du bist interessiert an den neuesten Entwicklungen und Trends in den Bereichen Bilderkennung, Natural Language Processing und Neuronale Netze? Du hast bereits Erfahrung in datengetriebener Modellierung?

Nimm die Herausforderung an und entwickle im Team eine einzigartige Data Science-Lösung. Dich erwartet ein spannendes Wochenende zusammen mit vielen motivierten Talenten in einem anregenden Umfeld. Triff interessante Leute, tausch Dich mit ihnen aus und miss Dich mit ihnen in einem Wettstreit um attraktive Preise.

Jetzt anmelden und mitmachen unter: http://hackathon.d-fine.com/

EINLADUNG ZUM »SCIENCE IN FINANCE«-WORKSHOP!

Wenn Sie sich fragen, wie die Bank Ihres Vertrauens die immer schneller werdende Abfolge von immer anspruchsvolleren regulatorischen Anforderungen durch mathematische Modellierung,

neue Prozesse und Big Data in die Praxis umsetzt, dann nehmen Sie die Rolle derjenigen ein, die diesen regulatorischen Tsunami für die europäische Finanzindustrie in den letzten Jahren beherrschbar gemacht haben: Lernen Sie d-fine kennen – nicht als Bewerber, sondern als Berater!

Erfahren Sie, wie Sie Ihren mathematischen Hintergrund und Ihre analytischen Fähigkeiten einbringen können, um die Stabilität der Finanzmärkte zu erhöhen. Als Berater in einem Projektteam von d-fine werden Sie für die d-fine Bank AG ein Modell entwickeln, um das Institut rechtzeitig in die Lage zu versetzen, die neuerlichen Bewertungsanforderungen der Aufsicht zu erfüllen – hierbei handelt es sich um eine Arbeit direkt aus der täglichen Praxis von d-fine. Erfahren Sie durch die Teamarbeit mit Ihren Kollegen/-innen und in der Interaktion mit den Abteilungen der Bank, wie herausfordernd und vielfältig die Arbeit eines d-fine Beraters ist!

d-fine ist ein führendes europäisches Beratungsunternehmen mit Standorten in Berlin, Düsseldorf, Frankfurt, London, München, Wien und Zürich. Mit über 700 hochqualifizierten Beratern unterstützen wir unsere Kunden aus Industrie, Finanzwelt oder öffentlicher Hand bei anspruchsvollen quantitativen, prozessualen und technologischen Herausforderungen. Strategieberatung, Fachberatung, Technologieberatung: d-fine ist alles in einem.

d-fine. analytisch. technologisch. quantitativ.

3-tägiger Workshop mit Vorträgen zur Finanzmathematik, einem Kundenprojekt unter Ihrer Beteiligung und Erfahrungsberichten aus unserer Consulting-Praxis.

Bewerbungsschluss: 10. September 2018

Termin. 7. bis 9. November 2018

Ort: Schlosshotel Kronberg im Taunus

Kontakt:

d-fine GmbH

Svenja Dröll

An der Hauptwache 7

60313 Frankfurt am Main

T +49 69 907 37- 555

Careers

MathFinance Openings

Senior Quant/ Consultant

We are looking for senior quant / consultant in the areas of

Insurance

- Actuary with 5 to 7 years of experience in insurance or re-insurance

- Experience in quantitative Risk Management in relation to regulatory issues (Solvency II)

- Experience in Capital Management

Banking

- Quant with 5 to 7 years of experience in Banking, ideally in Trading

- Experience in quantitative Risk Management in relation to regulatory issues (Basel III)

- Experience in Capital Management

Investment

- Quant with 5 to 7 years of experience in Asset Management (Funds, Insurance and Family Offices), ideally with emphasis on Risk Management

- Experience in quantitative Risk Management in relation to regulatory issues (German KAGB and KARBV)

Please send us your CV to recruitments@mathfinance.com

Junior Quant

Do the following apply to you?

- Master degree or diploma in (business) mathematics or physics

- PhD or CFA is a bonus

- First experiences in mathematical finance is desirable

- Very good programming skills, e.g. C++, Python or Matlab

- Good language skills in German and English

- Outstanding analytical skills and a problem-solving attitude

- High motivation to develop your knowledge and skills

- Good communication skills and team spirit

Then we would like to hear from you. Please send us your CV to recruitments@mathfinance.com